Key highlights

The Canadian debt market continued to experience sluggish overall growth in Q3. Year-to-date loan issuance was $1.35 trillion, driven primarily by the demand for new money. Loan issuance increased by 6.7% when compared to Q3 2023.

The real estate and financial services sectors made up the bulk of total lending in Canada, followed by retail and wholesale, and other professional services sectors. These four areas comprised almost 60% of total business lending in Canada.

Business sentiment remains muted due to subdued demand

Businesses continued to struggle with weak demand, excess capacity and slow price growth. Sales were slow and sales expectations continued to be soft in Q3 of 2024. This led to restrained investment and hiring. Many companies decided to replace or repair equipment and held off on increased capital spending. Labour was plentiful and expectations for growth in wages, input costs, and selling prices have continued to normalize.

The transportation and logistics sectors continued to struggle with the lower market demand, and manufacturing was also impacted. Financing conditions and a weaker economy created reduced demand for materials and machinery. Given reduced growth, the outlook these sectors remain sluggish.

Rates cuts on both sides of the border

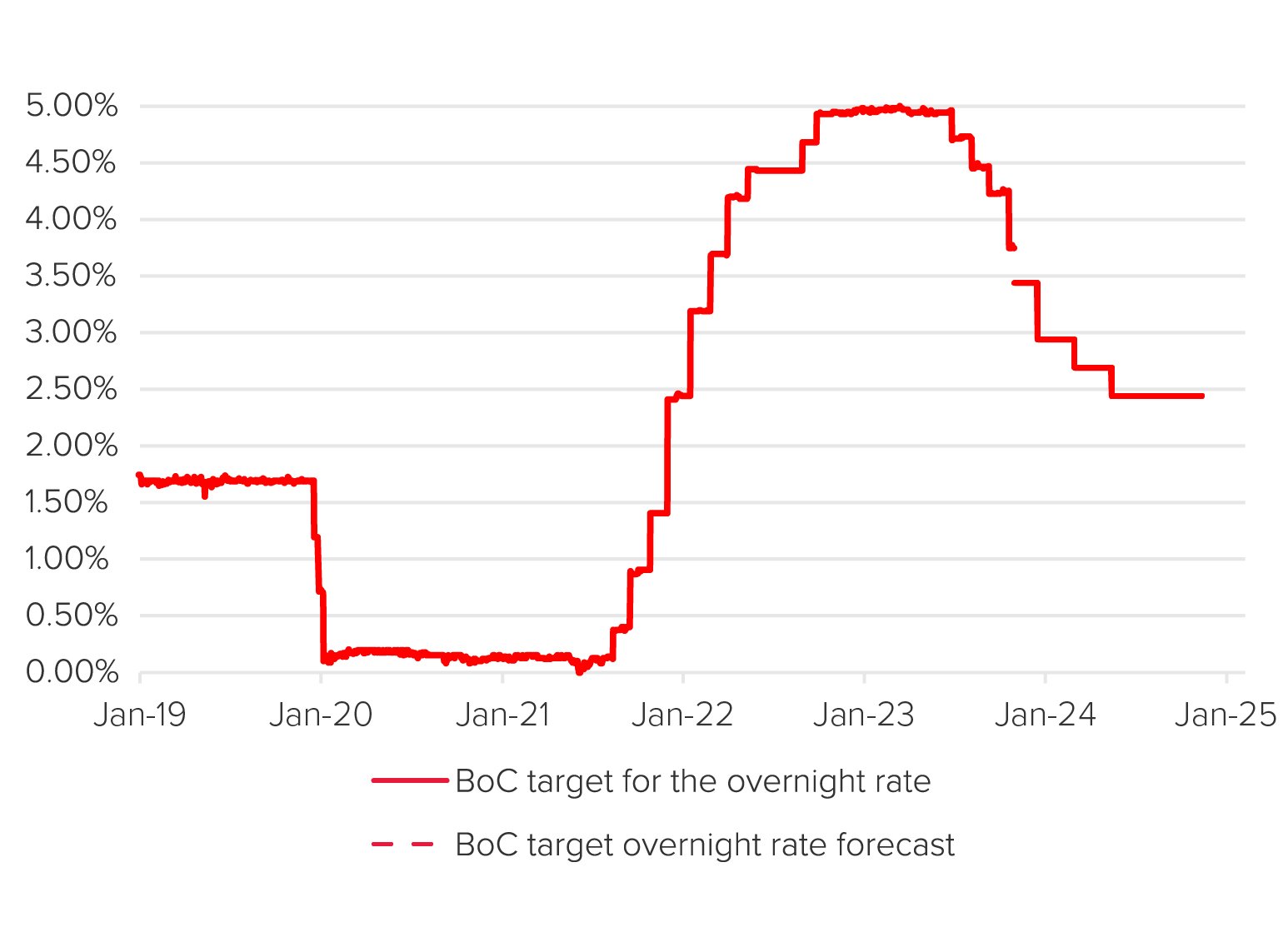

The U.S. Federal Reserve delivered a surprise jumbo 50-basis point rate cut in September. This was mostly triggered by a slowing job market and weaker inflation. The Bank of Canada followed with a 50-basis point rate cut in October to support economic growth and keep inflation close to 2%. Some economists and most businesses were hoping for a 75-basis point cut. But the Bank of Canada delivered as per market expectations.

However, given that inflation is a lagging indicator, the larger cut potentially raised the question of whether the central bank should have started its cuts sooner. Sectors hardest hit by higher interest rates were real estate and those impacted by consumer spending. The pace of declining rates will be determined in large part by the U.S. economy. Given the ongoing strength of the economy south of the border, the expectation is for the Bank of Canada to cut rates at a graduated pace.

Big banks report Q3 results and higher loan loss provisions

Canadian banks continue to be dependable during these economic times. Overall, RBC exceeded, National Bank, Scotiabank, and CIBC remained steady, BMO faltered, and TD continued to struggle with its anti-money laundering issues south of the border. Rising provisions for credit losses continued as a common theme. The losses were not focused on a particular sector and some banks implied the rising provisions were due to syndicated facilities both north and south of the border.

All the banks continue to focus on consolidation. However, RBC implied it was going to step away from U.S. acquisitions temporarily given how unique the American market is and instead focus on Canada. In terms of the state of past acquisitions, the one thing that stood out is the HSBC acquisition has been good for RBC. National Bank stated it was too early to speak about the pending CWB acquisition. The Canadian banks will need to continue focusing on integrating these acquisitions in order to realize the cost synergies.

Navigating a noisy autumn with all eyes on the impact of the U.S. election

Given the fact that Canada exports 75% of its goods and services to the U.S., the outcome of the election will impact the Canadian economy. Although there is discussion around renegotiation of tariffs, the U.S. will want to keep production activities closer to home and prevent supply chain issues that occurred during the COVID-19 pandemic. So all are watching closely to see if the new administration in the U.S. renegotiates policies/tariffs on Canada. The key impact will be the shift in the U.S. on oil and gas producing industries. Green incentives/policies will continue as planned, thereby leading to continued growth of industrial- and infrastructure-related construction. The one area to watch will be the U.S.-China relationship and its impact on the technology sector and availability of key goods like semiconductors, which impact the production of automobiles and electric vehicles.

Will the landing be soft as predicted?

A soft-landing scenario continues to be the more likely outcome in 2025. Overall, given high interest rates, weak demand, and a cautious financing environment, businesses should expect a gradual economic recovery, which will impact the pace of future business investment. The Bank of Canada’s continued efforts to lower interest rates will be crucial in supporting the recovery and steering the economy towards a more robust growth trajectory.

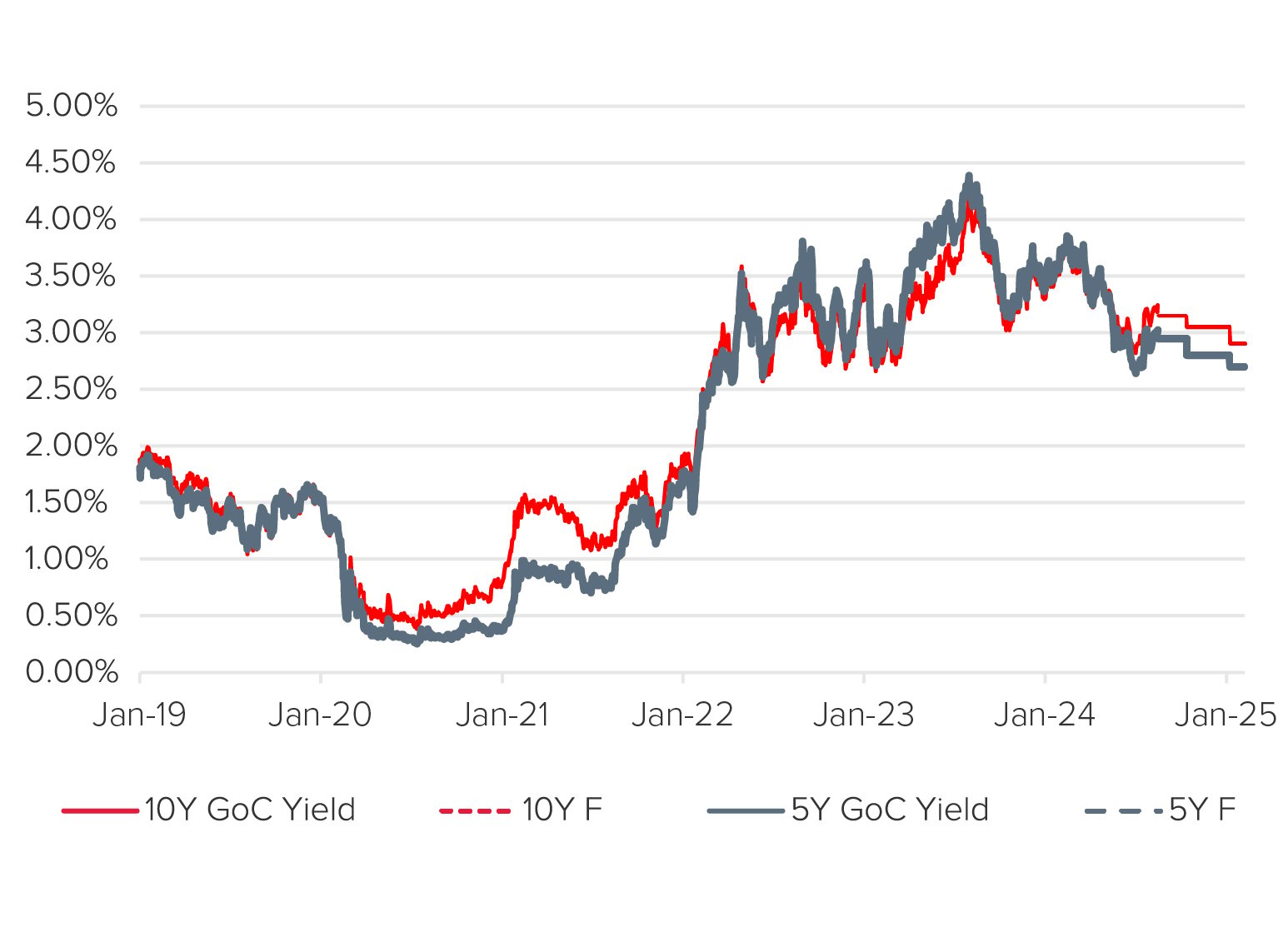

10Y GoC Yield vs 5Y GoC Yield

2019-2025F

Source: Statistics Canada and the Bank of Canada

BoC Target Rate

2019-2025F

Source: Statistics Canada and the Bank of Canada

| < $5M | > $10M | > $20M | |

|---|---|---|---|

| Jul 2024 | 1.75x - 2.75x | 3.00x - 4.00x | 3.50x - 4.00x |

| Aug 2024 | 1.75x - 2.75x | 3.00x - 4.00x | 3.50x - 4.00x |

| Sep 2024 | 1.75x - 2.75x | 3.00x - 4.00x | 3.50x - 4.00x |

Source: BDO, M&A and Capital Markets estimates

| < $5M | > $10M | > $20M | |

|---|---|---|---|

| Jul 2024 | 3.00x - 4.00x | 4.00x - 4.75x | 4.25x - 5.00x |

| Aug 2024 | 3.00x - 4.00x | 4.00x - 4.75x | 4.25x - 5.00x |

| Sep 2024 | 3.00x - 4.00x | 4.00x - 4.75x | 4.25x - 5.00x |

Source: BDO, M&A and Capital Markets estimates

| < $5M | > $10M | > $15M | |

|---|---|---|---|

| Jul 2024 | P+1.0% - 2.0% | P+1.0% - 2.0% | P+1.0% - 2.0% |

| Aug 2024 | P+1.0% - 2.0% | P+1.0% - 2.0% | P+1.0% - 2.0% |

| Sep 2024 | P+0.5% - 2.0% | P+0.5% - 1.5% | P+0.5% - 1.5% |

Source: BDO, M&A and Capital Markets estimates

| < $5M | > $10M | > $20M | |

|---|---|---|---|

| Jul 2024 | 11% - 15% | 10% - 15% | 10% - 13% |

| Aug 2024 | 11% - 15% | 10% - 15% | 10% - 13% |

| Sep 2024 | 11% - 15% | 10% - 15% | 10% - 13% |

Source: BDO, M&A and Capital Markets estimates

Capital Advisory overview

Our Capital Advisory team works with companies to find the right capital solution for their business. We have relationships with commercial banks, alternative lenders, private equity firms, and other capital/debt financing providers in Canada, the U.S., and globally, which allows us to find financing that aligns with client objectives.